.jpg?fit=crop&w=280&h=280&q=93)

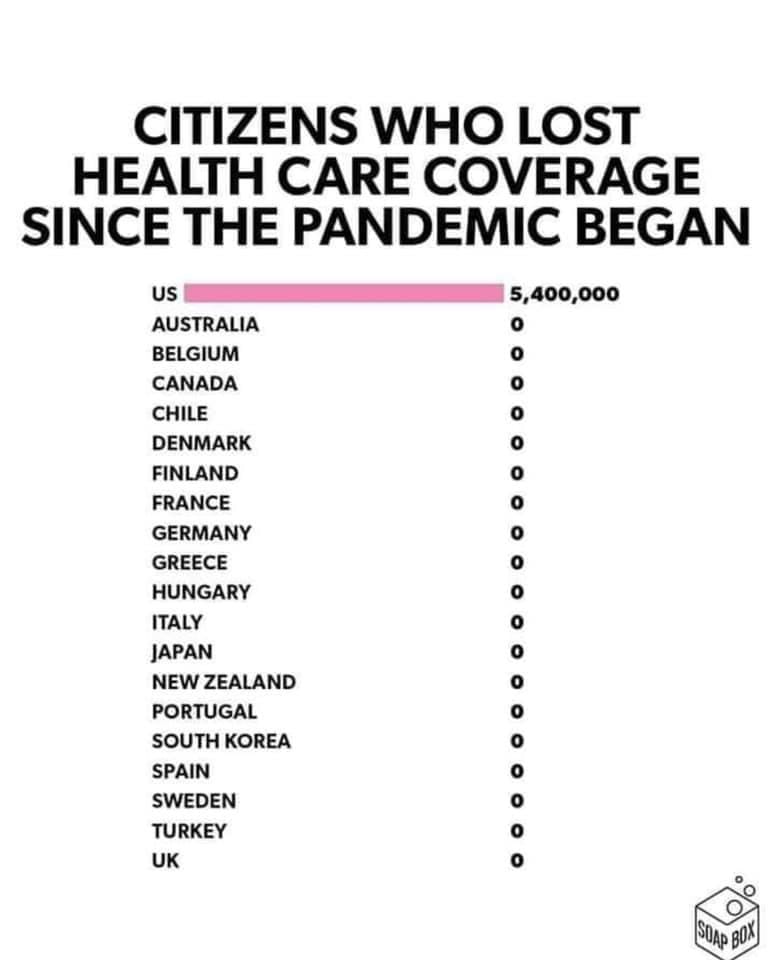

There is still time to enroll for individual health insurance! Washingtonians have until January 15th to get coverage starting February 1, 2021. The attached Newsletter has information about the health insurance companies, counties they serve, provider networks and tax subsidy/reduced rate info. Click the photo below to go to the Exchange and can create an account. For my assistance, go to Quick Links and "Find a Broker" and type "Suderman" in the last name field and confirm your request. I will then be notified so we can connect. There is no charge to you for this service.

.jpg?fit=crop&w=200&h=200&crop=faces)

- Copy.jpg?fit=crop&w=280&h=280&q=93)